David R. Hines, CFA

David R. Hines, CFA

Volatility has returned to the equity markets after being abnormally low through the summer months. Rather than react emotionally to volatility we remain disciplined in our process which focuses on the fundamental drivers of value(1). In this note we will put volatility in context, check to see if any long-term fundamentals have changed, and determine if any portfolio actions are necessary.

The last time we were compelled to draft a note addressing volatility was September 1st, 2015. At that time, falling oil prices and slowing growth in China were among the perceived risks of the day. Valuations were high (P/E of the S&P 500 was 19x), income yields were historically low (10-year US treasury was 1.6%), and earnings growth (1.4% year-over-year EPS growth) was anemic. We recommended that equities still offered the best relative value and advised clients not reduce their equity allocations. This was good advice. The S&P 500 is 50% higher (even after October’s drop) today while most bond returns have barely kept up with inflation!

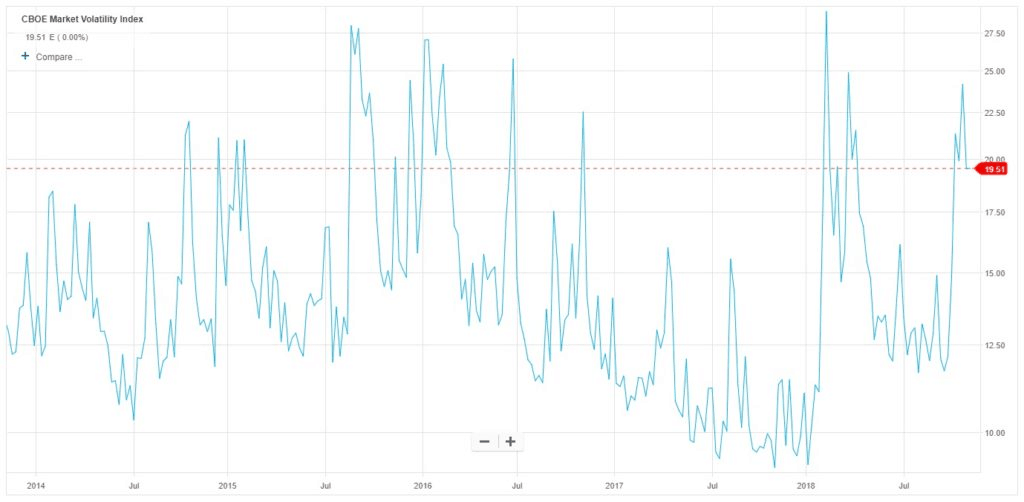

We acknowledge the sudden drop in equity prices in October was steep, even by historical standards. The S&P 500 was in correction territory (10% decline from previous high) by late October for the second time this calendar year. In fact, this was the sixth market correction since the bull market began in March of 2009. Drivers of this recent volatility include uncertainties surrounding trade deals, higher interest rates, and global growth concerns. The VIX(2), a measure of perceived risk in the S&P 100, rose dramatically. The VIX has spent much of the last 5 years tracking below 15 but recently spiked to 25. As the chart below shows, periods of volatility have been quite common over the last 5 years and have typically been short-lived.

CBOE Market Volatility Index, Q4 2014-Present

Volatility in stocks is never fun but it is normal. It is the price one pays for higher longer-term returns. In consideration of funding near-term liabilities, volatility does matter most. But, it is not the only risk. To meet obligations well into the future, achieving real (inflation adjusted) portfolio total returns is the most important, and managing short-term volatility much less so. In between the long and short-term, portfolio cash flow (income) matters most. Our investment process addresses each of these risks.

Two important elements of total return are growth and valuation. By some traditional measures equity valuations continue to look high(3) even as strong earnings growth this year has brought valuations down. The current 2019 consensus earnings estimate for the aggregate companies in the S&P 500 is around $170 per share(4). The recent level of the S&P 500 is 2658. This produces a forward-looking price-to-earnings ratio of 16x compared to over 18x just a year ago. This valuation level may even be considered cheap in the context of low interest rates and low capital gain tax rates. Companies continue to have access to low cost capital and their profit margins remain wide.

An often-cited concern is that earnings growth has peaked and will start slowing. While this may be true, we do not find evidence this will cause distress in company cash flows or dividends. We can look to bond credit markets for signs of cash flow distress. Risky bond indexes that contain high yield bonds and leveraged loans have held steady even as equity indexes have fallen. The credit markets do not suggest there is reason for concern regarding the sustainability of corporate cash flows.

We have written about planning for volatility in the past and use asset allocation as a way to manage this risk. As in any market, we suggest looking at spending needs over the next 3 to 5 years using cash or short-term bonds. One factor that has changed this year is the opportunity cost of holding cash has dropped. With yields at or near 2% and rising, money market funds provide returns close to medium-term and long-term bonds.

Uncertainties regarding earnings growth, trade tensions, and rising interest rates are re-awakening stock market volatility. Balancing these issues are strong economic numbers and stable forward earnings estimates. As volatility rises we do not deviate from our core portfolio construction process. Our portfolios have cash and bond allocations knowing that volatility will inevitably rise at times. Our research process focuses on company fundamentals and valuation characteristics that produce compounding cash flows over time. As always, we encourage you to contact your HM Payson team with any questions or concerns.

(1) It is important to note that price and value may diverge significantly in the short term. Price is simply the current market quotation while value is derived from a combination of cash flows, growth, and a discount rate.

(2) The Volatility Index or VIX is a mathematical measure of how much the market thinks the S&P P 100 Index option, or OEX, will fluctuate over the next 12 months, based upon an analysis of the difference between current OEX put and call option prices.

(3) The market continues to look expensive when using price to sales and price to book value measures.

(4) Source: FactSet as of October 26, 2018